Assisted living fee negotiation is the practice of reducing or eliminating specific upfront and recurring charges before signing a residency contract. Most families assume the monthly rate on a brochure is fixed. It is not entirely. This negotiating assisted living fees guide explains exactly which costs bend, which do not, and how to use timing, occupancy data, and contract knowledge to protect your family’s finances without compromising your loved one’s care.

Which assisted living fees are negotiable and which are fixed?

Negotiation success depends more on understanding which cost components are flexible than on aggressive bargaining over monthly rates. That single insight separates families who save thousands from those who walk away frustrated.

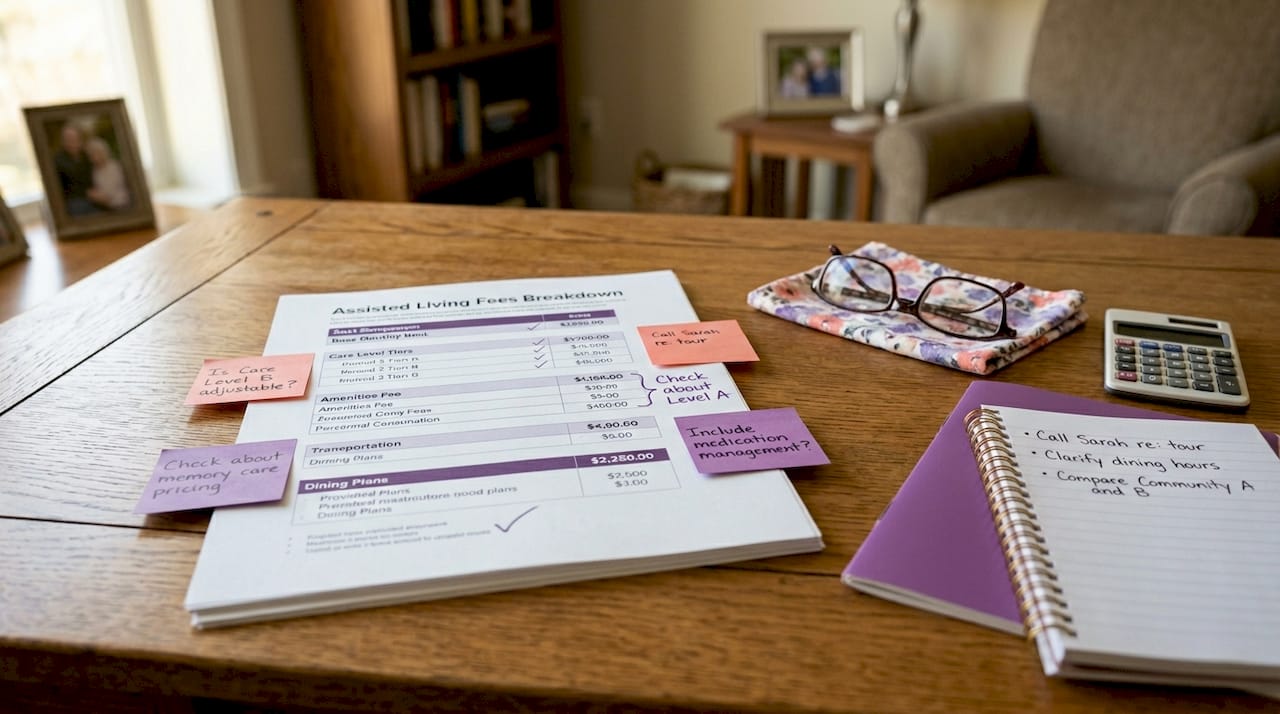

The assisted living pricing model is modular, not monolithic. Think of it as three layers stacked on top of each other: a base monthly rent, tiered care fees tied to Activities of Daily Living (ADLs), and add-on service charges. Unadvertised fees and tiered care levels often add over $1,000 per month beyond base monthly rent. That means the number in the brochure can be a fraction of what you actually pay.

Here is how the negotiable and fixed categories break down:

| Cost Item | Negotiable? |

|---|---|

| Move-in or community fee | Yes. Often waivable or reducible. |

| First month’s rent discount | Yes. Common during slow seasons. |

| Base monthly rent | Rarely. Discounts are usually temporary. |

| Tiered care level fees | No. Set by nursing assessment of ADLs. |

| Add-on service charges | Sometimes. Bundling can reduce per-item cost. |

Move-in fees commonly range from $1,000 to $15,000, and waivers or reductions on these fees can produce significant upfront savings. Always request a full written cost breakdown that includes base rent, every care tier, and all add-ons before entering any price discussion. Communities that refuse to provide this in writing are telling you something important about how they operate.

Pro Tip: Ask for the fee schedule in writing before your first formal tour. Reviewing it in advance gives you specific line items to question rather than reacting to a sales presentation.

How does timing affect your negotiating leverage?

The national average occupancy rate for assisted living communities sits at approximately 87%, which means most facilities carry some vacancies at any given time. Lower occupancy and slower seasons improve negotiation chances directly. A community with empty units has a financial incentive to fill them, and that incentive is your leverage.

Four timing windows consistently produce better outcomes:

- Winter months (November through February). Move-in rates slow seasonally, and communities are more willing to offer incentives to maintain occupancy.

- New community openings. Pre-opening and lease-up phases often include promotional pricing to hit occupancy targets quickly.

- Quarter-end periods. Sales staff working toward quarterly targets have more authority to approve discounts or waive fees.

- After a rate increase notice. If a community has just raised rates, they may offer concessions to retain residents and avoid vacancies from departures.

Timing moves to coincide with lower occupancy, slow seasons, and quarter-end periods can produce meaningfully better outcomes because communities face real operational and financial pressure to fill beds. When you approach a director of sales during a slow period with a competing quote in hand, you are negotiating from a position of strength, not desperation.

Always ask to speak with the executive director or director of sales directly. Front-line staff rarely have authority to approve fee waivers. Going to the right decision-maker shortens the process and signals that you are a serious, informed buyer.

What contract terms should you review before signing?

Contract clauses controlling reassessments and care levels dictate long-term affordability more than initial prices. A low move-in rate means little if the contract allows unlimited rate increases with minimal notice.

Watch for these specific clauses:

- Rate increase provisions. Some states require 90 days’ written notice for assisted living rate increases, but many contracts allow shorter notice periods. Push to negotiate the notice period to at least 60 days and request a cap on annual increases.

- Care level reassessment triggers. Facilities set additional charges based on nursing assessments of ADLs, which can raise monthly fees substantially if care needs increase. Negotiate for written criteria that define when a reassessment occurs and who conducts it.

- Discharge provisions. Some contracts allow a facility to discharge a resident with limited notice if care needs exceed what the community provides. Understand the exact threshold and notice period before signing.

- Medicaid transition language. If there is any chance your loved one will eventually rely on Medicaid, confirm the contract does not contain a clause that terminates residency upon Medicaid enrollment.

“Verbal incentives are only effective when documented. An elder law attorney review is recommended to spot problematic contract clauses and ensure financial protections.” — Care.com

Engaging both a senior living placement advisor and an elder law attorney before signing is the most powerful negotiation strategy available to families. The placement advisor uncovers unpublished incentives; the attorney flags risky contract language. Using only one of these resources leaves money or protection on the table. You can find guidance on preparing for the move through Assistedlivingadvisers, which includes contract review considerations specific to the tri-state area.

What questions should you ask when touring a community?

The tour is your primary discovery tool for assisted living cost negotiation. Most families use it to evaluate amenities. Savvy families use it to surface every cost and contract risk before any emotional attachment forms.

Ask these questions on every tour:

- What is the full monthly cost at each care level, and what triggers a move between levels?

- Is the community fee or move-in fee negotiable, and what promotions are currently available?

- What services are included in the base rate, and which carry additional charges?

- How often are care reassessments conducted, and who performs them?

- Does the community accept Medicaid, and if so, how many Medicaid beds are available?

- What is the notice period for rate increases, and what is the average annual increase over the past three years?

- Are there restrictions on bringing in outside home care agencies to supplement services?

Touring assisted living communities should function as a structured discovery process to get accurate pricing and contract details, not just a facility walkthrough. Question seven matters more than most families realize. Some communities prohibit or restrict outside care providers, which forces you to purchase all additional services at their rates. That restriction can cost thousands per month as care needs increase.

You can use Assistedlivingadvisers’ resource on comparing assisted living communities to build a side-by-side cost comparison across multiple communities before your tours begin.

How does Medicaid affect assisted living costs and what other options exist?

Medicaid HCBS waivers may cover care services in assisted living but not room and board. This distinction is critical for budgeting. Medicaid can reduce the care portion of your monthly bill, but the housing cost remains your responsibility.

Key facts about Medicaid and assisted living in 2026:

- The Federal Benefit Rate (FBR) is $994 per month for individuals. Many states set Medicaid income eligibility at 300% of that figure, or approximately $2,982 per month.

- Not all facilities accept Medicaid. Upfront verification of acceptance and associated costs is required for accurate budgeting.

- Facilities that accept Medicaid often cap the number of Medicaid beds available, so placement is not guaranteed even if your loved one qualifies.

- Spend-down rules allow individuals with income above the threshold to qualify by deducting medical expenses from countable income.

| Financial Option | What It Covers | Key Limitation |

|---|---|---|

| Medicaid HCBS Waiver | Care services only | Does not cover room and board |

| Long-term care insurance | Both care and housing, depending on policy | Requires prior enrollment; benefit caps apply |

| Veterans Aid and Attendance | Monthly benefit for qualifying veterans | Income and asset limits; application process is lengthy |

| Irrevocable Medicaid trust | Protects assets while qualifying for Medicaid | Must be established at least 5 years before application |

Long-term care insurance policies vary significantly in what they reimburse. Review the daily benefit amount, elimination period, and inflation protection rider before assuming a policy covers the full cost. For families exploring how to pay for assisted living, Assistedlivingadvisers provides a detailed breakdown of payment options specific to New York, New Jersey, and Connecticut.

Key takeaways

Effective assisted living fee negotiation targets upfront and contract-level costs, not monthly rates, and requires legal review, timing awareness, and Medicaid planning to protect long-term affordability.

| Point | Details |

|---|---|

| Target flexible fees first | Move-in and community fees are the most negotiable items; monthly rates rarely change permanently. |

| Use occupancy as leverage | An 87% national average occupancy rate means most communities have vacancies and financial incentive to negotiate. |

| Prioritize contract clauses | Rate increase notice periods and reassessment triggers control long-term costs more than initial pricing. |

| Document everything | Verbal promises have no legal weight; get every incentive and concession in writing before signing. |

| Verify Medicaid early | Not all facilities accept Medicaid, and coverage excludes room and board in most states. |

What I’ve learned after years of watching families negotiate these fees

Most families walk into assisted living negotiations focused entirely on the monthly rate. That instinct is understandable. The monthly number is the biggest and most visible cost. But it is also the hardest to move. Communities price their base rates to reflect market positioning, and a permanent monthly discount is almost never on the table.

Where I consistently see families win is on the front end. A waived community fee of $5,000 is real money. A free first month is real money. A written guarantee that the annual rate increase will not exceed 5% is worth more than any one-time discount. These are the terms worth fighting for, and they are achievable because they cost the community less than a prolonged vacancy.

The other mistake I see repeatedly is skipping the elder law attorney. Families spend weeks comparing amenities and then sign a 20-page contract in a single afternoon. That contract may include a reassessment clause that allows the community to move your loved one to a higher care tier with 48 hours’ notice and no independent review. An elder law attorney in New York or New Jersey charges a few hundred dollars for a contract review. That fee has saved families tens of thousands of dollars in unexpected cost escalations.

My honest advice: treat the contract negotiation as seriously as the fee negotiation. The monthly rate you agree to on day one matters far less than the rules governing how that rate can change over the next three years.

— Eric

How Assistedlivingadvisers can help you negotiate and place with confidence

Families working with Assistedlivingadvisers gain access to local expertise across New York City, New Jersey, and Connecticut at no cost. The team identifies communities with current vacancies and unpublished move-in incentives, compares fee structures across vetted options, and coordinates tours so you arrive prepared with the right questions.

Assistedlivingadvisers also connects families with elder law attorneys who specialize in reviewing assisted living contracts before signing. Whether you are managing Medicaid planning, evaluating long-term care insurance, or simply trying to understand a fee breakdown, the guidance is personalized and free. Start by finding assisted living near you and scheduling a free consultation with the Assistedlivingadvisers team today.

FAQ

What fees are most negotiable in assisted living?

Move-in fees and community fees are the most negotiable items, with waivers or reductions saving families $1,000 to $15,000 upfront. Monthly base rates are rarely reduced permanently.

When is the best time to negotiate assisted living costs?

Winter months, quarter-end periods, and new community openings offer the strongest leverage because occupancy pressure gives communities a financial reason to offer concessions.

Does Medicaid cover assisted living room and board?

No. Medicaid HCBS waivers cover care services in assisted living but not room and board, and not all facilities accept Medicaid residents.

Why should I have an elder law attorney review the contract?

Contract clauses on rate increases and care reassessments can trigger significant cost escalations with minimal notice. An elder law attorney identifies and negotiates these risks before you sign.

What questions should I ask about care level fees during a tour?

Ask what triggers a care level reassessment, who conducts it, and what the fee increase is at each tier. Families who attend reassessments and request documentation prevent unnoticed cost increases over time.

Recommended

Let’s Work Together To Find The Ideal Senior Living Community For Your Loved One.

Assisted Living Advisers is a FREE, personalized service offering expert guidance in determining the ideal community for your loved one based on physical needs, location preferences and finances.